GRIFFEN THORNE

Cannabis regulation efforts are usually sold to voters or legislators with the express promise that a state will be able to milk the new industry for all it’s got through cannabis taxes. Don’t believe me? Well, look no further than California’s landmark Proposition 64, also known as the Control, Regulate and Tax Adult Use of Marijuana Act. Prop. 64’s third finding and declaration states explicitly that:

Table of Contents

Currently, marijuana growth and sale is not being taxed by the State of California, which means our state is missing out on hundreds of millions of dollars in potential tax revenue every year. The Adult Use of Marijuana Act will tax both the growth and sale of marijuana to generate hundreds of millions of dollars annually.In other words, from the inception, these programs were designed in large part to raise revenue for the state. And the state does so by funneling money out of the nascent industry in an extremely aggressive way – which is why I (only sort of hyperbolically) called this theft last year. California is not alone in this, and there are certainly many other states with regressive and punitive tax schemes that all but guarantee the tax-free illegal market will thrive. But California is a prime example of failed policy which legislators and regulators seem intent on making worse. Here’s why.

California’s cannabis tax scheme was destined to fail from the start

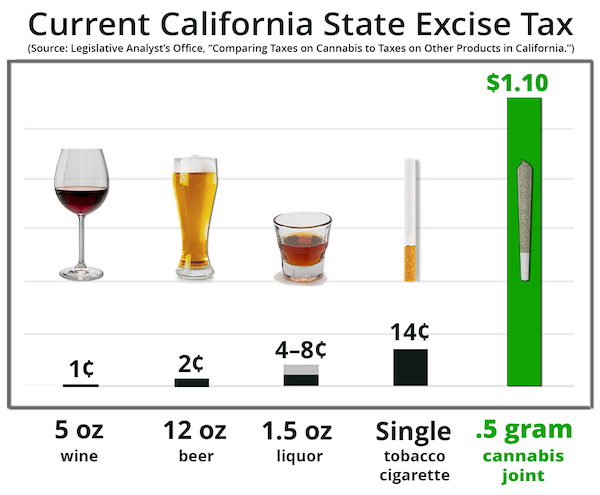

From inception, California decided to tax cannabis at both ends by imposing a tax on cultivated plants, and an excise tax on retail. This is in addition to sales tax, with a 7.25% sale price baseline and additional local add-ons. To make matters more, unnecessarily complicated, these taxes were not paid by cultivators and retailers, but by middlemen distributors. This meant that distributors constantly had to deal with tax issues on both ends of a delivery and hope they didn’t get stiffed. Lots and lots of distributors racked up late bills, to which the California Department of Tax and Fee Administration (CDTFA) tacked on 60% late fees and interest. I am not kidding there. As I noted last year, “Before the cultivation tax was eventually eliminated, it effectively was $161 per pound!” This was clearly not a sustainable situation for the industry. California finally got some sense and did away with the cultivation tax, but only on a prospective basis– meaning those distributors with massive tax bills got no real relief. Additionally, California passed off the excise tax remittance obligation to retailers, but in doing so, effectively imposed double taxation on them. Here’s an image that California NORML published to illustrate:

Credit: Here

Last year, I wrote this about the situation:

California’s cannabis tax regime is a failed experiment. Every time a legitimate, licensed business shuts its doors, statewide cannabis taxes are at least partially to blame. Until the state takes a hard and serious look at the issue, don’t expect much to change without people taking the state to court and holding them to task.

The above is just excise tax, to be clear. For any sale of cannabis, the excise and sales taxes alone will amount to at least 22.5%. That’s $22.50 on a $100 bill in just state cannabis taxation. A piece of proposed California legislation would have attempted to streamline some of the state level taxes to avoid double taxation, but it looks like the bill won’t advance much further. This is pretty terrible news during the midst of a literal crisis within the state’s cannabis industry.That proposed bill was held in a legislative committee and went nowhere. Right now there is no relief and these problems persist. Maybe the legislators will figure things out in the next few months, but let’s not be overly hopeful given the state’s track record.

California tries to raise cannabis taxes yet again

Last year, CDTFA promulgated an “emergency” regulation regarding the excise tax. Without getting too far into the weeds, the rule would change the metric for determining gross receipts for the sale of cannabis products sold at retail, and would do so in a manner that would end up increasing cannabis taxes. Catalyst, a California cannabis retail company, recently sued the CDTFA to find that the emergency regulation violates state law. To summarize one of the claims in their suit, if a vape pen retails for $40, but only has $5 of oil in it, state law only imposes a cannabis tax on the oil ($5) and not on the non-oil things. But under the new law, the tax would be payable on the entire $40. And this, Catalyst argues, violates state law. It’s not really clear why CDTFA decided to make this move and suddenly increase taxes for otherwise compliant operators, when so many licensed businesses are already so far in the hole. But it highlights the fact that the state is less interested in supporting its struggling industry than it is on taxing it.California uses cannabis taxes as a piggybank

In Prop. 64, voters were promised that cannabis taxes would be used as follows:The revenues will cover the cost of administering the new law and will provide funds to: invest in public health programs that educate youth to prevent and treat serious substance abuse; train local law enforcement to enforce the new law with a focus on DUI enforcement; invest in communities to reduce the illicit market and create job opportunities; and provide for environmental cleanup and restoration of public lands damaged by illegal marijuana cultivation.Despite the fact that California pretends to care about fixing cannabis taxes, it doesn’t. For example, the state’s AG said cannabis taxes would be lower five months ago, and that shockingly hasn’t happened. In fact, no relief is even on the table. Instead, the proposed budget will actually take a “loan” of $100 million from the cannabis tax fund to redirect to balance the state’s $38 billion budget deficit:

To address the projected budget shortfall, the Budget proposes General Fund solutions to achieve a balanced budget. This includes a budgetary loan of $100 million from the Board of State and Community Correction’s Cannabis Tax Fund subaccount to the General Fund from currently unobligated resources. See the Criminal Justice and Judicial Branch Chapter for additional information.If you expect that “loan” to ever be repaid, I’ve got a bridge to sell you. What’s more likely – in fact much more likely – is that these “loans” will become more commonplace in the future and that the state will magically forget about ever doing anything to reduce the tax burden on lawful operators so that it has this piggybank.

California’s cannabis tax regime is a failed experiment. Every time a legitimate, licensed business shuts its doors, statewide cannabis taxes are at least partially to blame. Until the state takes a hard and serious look at the issue, don’t expect much to change without people taking the state to court and holding them to task.